Tax in the Bluegrass

Kentucky Local Occupational License Taxes

Issue 5

December 20, 2022

By Mark A. Loyd, JD, CPA

The prevalence of occupational license taxes on wages and net profits imposed by local tax districts in Kentucky underscores Kentucky local tax districts’ dependence on these taxes for revenue. The Commonwealth has historically been dependent on taxes based on income as well but has recently moved away from income-based taxes to become more competitive. Local occupational taxes are significant. For Kentucky to become competitive, should not local taxes be addressed as well?

The prevalence of occupational license taxes on wages and net profits imposed by local tax districts in Kentucky underscores Kentucky local tax districts’ dependence on these taxes for revenue. The Commonwealth has historically been dependent on taxes based on income as well but has recently moved away from income-based taxes to become more competitive. Local occupational taxes are significant. For Kentucky to become competitive, should not local taxes be addressed as well?

Kentucky Constitution Section 181, state authorizing legislation, and local enabling acts

Counties and localities in Kentucky can only impose local occupational license taxes on wages and profits with the General Assembly’s authorization made pursuant to Section 181 of the Kentucky Constitution, as Kentucky Courts have repeatedly recognized. City of Louisville v. Sebree, 214 S.W.2d 248 (Ky. 1948); Second St. Properties, Inc. v. Fiscal Court of Jefferson Canty., 445 S.W.2d 709 (Ky. 1969); Meadows Health Systems East, Inc. v. Louisville/Jefferson canty. Metro Revenue Comin, 375 S.W.3d 71 (Ky. App. 2012). Because there are well over 200 tax districts that now impose occupational license taxes, it is no surprise that the General Assembly long ago enacted statutes like KRS 68.180, KRS 68.197, KRS 68.198, KRS 91.200 and KRS 92.281 to authorize counties and localities to enact ordinances imposing occupational license taxes on wages and net profits. These enabling statutes may also include limitations on the rate of tax, generally in the form of a “not to exceed” provision. School boards may also impose occupational license taxes. KRS 160.605. Counties and localities implement this authority by enacting occupational license tax ordinances. Some revenue departments of tax districts, like Louisville Metro Revenue Commission (LMRC), for example, have promulgated regulations concerning their occupational license taxes.

Not all of Kentucky’s 120 counties and not all localities have imposed occupational license taxes. Approximately 90 Kentucky counties impose occupational license taxes, according to the Kentucky Association of Counties (Chaco). 2019 County Tax Snapshots available at www.kaco.org/articles/2019-county-tax-snapshots/. Oldham County, for example, does not impose an occupational license tax.

Kentucky localities’ occupational license taxes on wages and net profits

Occupational license taxes, as noted, generally take two forms, taxes on wages and taxes on net profits.

Local occupational license taxes on wages are imposed on salaries, wages, commissions, and other compensation earned by persons within the tax district for work done and services performed or rendered in that jurisdiction. Compensation includes not only salaries and wages but also certain benefits. KRS 67.750. Regardless of whether an employee is a resident or nonresident of the tax district, tax is imposed only on compensation for work done in that jurisdiction. This is generally accomplished by multiplying an employee’s total wages by a fraction whose numerator is the days spent on the job in the tax district and whose denominator is the total days spent on the job by the employee everywhere, with the amount resulting from this calculation being treated as the wages subject to tax. See, e.g., LMRC Reg. §1.05.A. Employers are required to deduct and withhold occupational license tax. KRS 67.780. Employees may request a refund when an employer withholds tax on compensation attributable to activities performed outside the tax district. KRS 67.788.

Local occupational license taxes are also imposed on net profits of businesses, trades, professions, or occupations from activities conducted in the tax district. Net profits are determined by reference to taxable income under the federal Internal Revenue Code as in effect on December 31, 2008. Obviously, the reference to the Code is, however, long overdue for an update. Businesses with payroll and sales in more than one tax district generally apportion their net profits by applying an apportionment percentage comprised of an equally weighted payroll factor (with a numerator of payroll in the district and a denominator of payroll everywhere) and a sales factor (with a numerator of sales in the district and a denominator of sales everywhere). KRS 67.753. If the standard apportionment percentage does not fairly represent the extent of the business entity’s activity in the tax district, the business entity may petition the tax district or the tax district may require alternative apportionment. KRS 67.753.

Notably, in Meadows Health, a taxpayer attempted to challenge the inclusion of capital gains from the sale of business assets as net profits subject to the local occupational license based on Section 181. But, the Kentucky Court of Appeals rejected the challenge, finding nothing in Section 181, the enabling statute or the relevant ordinances precluded the inclusion of capital gains in the tax base.

Obviously, the tax base and business net profits tax apportionment are different from the Kentucky income tax base which is based on the Code effective as of December 31, 2021, and apportioned using a single sales factor apportionment percentage using market-based sourcing. KRS 141.010 & KRS 141.120.

Tax district revenues from occupational license taxes

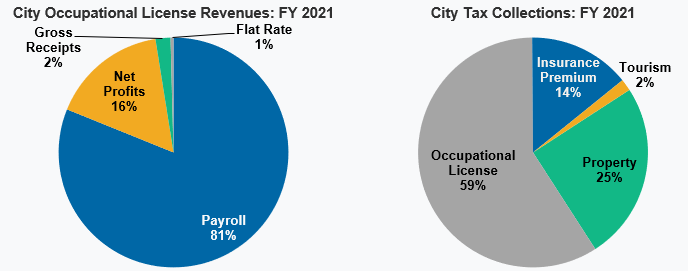

Occupational license taxes comprise a significant portion of city revenues (59 percent), according to 2021 data compiled by the Kentucky League of Cities, and noting also that most tax collections are from wage (payroll) taxes (81 percent) as compared to net profits taxes (16 percent).

www.klc.org/InfoCentral/Detail/31/occupational-license-tax

“Occupational license tax revenue [as of 2019] makes up nearly forty percent of all county tax revenue. Real estate property taxes come in second with 29 percent of revenue and insurance premium taxes are a distant third with 8.4 percent of revenue.” KACo 2019 County Tax Snapshots.

Major compliance challenges for taxpayers

Occupational license taxes imposed by Kentucky local taxes are outliers for multiple reasons. First, few states have localities that impose income taxes. “Fifteen states tax either personal or business income at the municipal level, and only eight—including Kentucky—tax both.” Tax Foundation, Aligning Kentucky’s Tax Code for Growth (2021) (available at taxfoundation.org/kentucky-tax-reform/). Second, the sheer number of tax districts (120 counties alone) in a state the size of Kentucky increases the complexity of compliance for businesses with occupational license tax obligations in multiple tax districts. Third, while most states, including Kentucky, are moving toward single sales factor apportionment using market-based sourcing, Kentucky’s local tax districts use a two-factor apportionment formula that gives the payroll factor a 50 percent weight, more than any other taxing jurisdiction, which creates complexity in compliance and serves as a disincentive to locate employees in tax districts levying an occupational license tax on net profits. And, the local occupational license tax base is wholly disconnected from the federal income tax base, since the reference to the Internal Revenue Code is roughly 14 years out of date.

Not surprisingly, business taxpayers, especially small businesses, face major challenges in trying to comply with local occupational license taxes in Kentucky.

- Identifying obligations to file in local tax districts. With over 200 tax districts, it is not straightforward for business taxpayers to identify which counties and localities impose occupational license taxes.

- Cost of preparing and filing tax returns in dozens or hundreds of tax districts. It is costly to prepare or pay to have prepared local occupational tax returns. It is commonplace for the cost of preparation and filing to exceed the local tax obligation.

- Complexities of complying with different tax bases and different apportionment formulas. Different tax bases and apportionment formulas require the collection and analysis of data specifically for local occupational license tax returns that would not otherwise be required and is not intuitive as such is different from that required for Kentucky state income tax returns.

Because employers are responsible for computing, withholding and paying occupational license tax on wages, employees themselves do not generally face the same challenges as their employers.

Shift to tax base and apportionment consistent with those of the Commonwealth?

The first simplification of the occupational license tax base and apportionment began in 2003, though it was not effective until mid-2008 when the provisions of KRS 67.750 to KRS 67.790 became effective. These provisions provided for a statewide uniform occupational license tax base starting with the Internal Revenue Code (with certain adjustments) and for a statewide uniform two-factor apportionment formula.

Since then, however, the local occupational license tax reference to the Internal Revenue Code has not been updated. Would it not be much simpler to comply if the Code reference date was updated to the current Internal Revenue Code? Perhaps the Code reference in KRS 67.750 could be linked to the reference in KRS 141.010? Moreover, the local tax district two-factor apportionment formula has not been updated to conform to the Kentucky single sales factor apportionment formula. Would it not be much simpler for taxpayers to comply using a single sales factor apportionment formula for their net profits taxes consistent with that used to compute state income taxes? Again, perhaps KRS 67.750 could reference the statewide apportionment factor in KRS 141.120?

Move to centralized filing for multijurisdictional filers?

With hundreds of local tax districts in Kentucky imposing occupational license taxes and the trend toward hybrid work and remote work, the burden of preparing multiple tax returns and filing in multiple tax districts has increased markedly. The costs are high for businesses.

Before 2012, the most comprehensive list of occupational license taxes was kept by the Kentucky Society of CPAs. However, legislation enacted in 2012 required the Kentucky Secretary of State to create and maintain a centralized repository of local forms, instructions and ordinances. KRS 67.766. These may be found at web.sos.ky.gov/occupationaltax/. Taxpayers may use Form OL-S, Single Tax District Standard Occupational License Fee Return and Form OL-D, Dual Tax District Standard Kentucky Local Occupational License Fee Return, which are uniform forms. Some tax districts, however, require preparers of multiple forms (e.g., 25 forms or more) to file electronically with the tax district. See, e.g., LMRC Reg. §1.18.A. Is this inconsistent with KRS 67.767?

It would seem to make it much more straightforward for taxpayers to identify which tax districts impose occupational license taxes if there was a single point of filing and payment for both wage and net profits taxes. Would it not make it much less expensive to prepare tax returns and file them as well, especially with a uniform tax base and a simple single sales factor apportionment? This could be a win-win with less cost for business and more compliance meaning more tax revenues for tax districts.

Shift away from local wages and net profits taxes?

As the Commonwealth shifts away from income taxes, does it not make sense for local tax districts to also shift away from income taxes? In a few years, provided that state individual income tax rates decline as anticipated, local income-based occupational license taxes can be anticipated to be more significant that state income taxes. 2022 Ky. Acts, c. 212.

For individuals, local taxes can be a significant burden. For example, the wages of a Louisville Metro resident employee working in Jeffersontown in Jefferson County is taxed at a rate of 2.2 percent (Metro Revenue, Mass Transit and School Board) plus 1 percent (Jeffersontown) for a combined rate of 3.2 percent. This poses a disincentive for businesses to locate employees in a local tax district, especially when they can be located elsewhere, which is even easier with the prevalence of remote work.

Likewise, local net profits taxes can also be a significant burden as the rate on a business taxed on its net profits would also be subject to a 3.2 percent rate, especially for businesses with employees in a local tax district, which increases a business’s payroll factor percentage and thus its apportionment factor. The payroll factor is a disincentive to locate in a local tax district.

As the Commonwealth reduces its dependence on income taxes to make Kentucky more competitive, should not localities shift away from income taxes as well? Perhaps phased in over multiple years? Obviously, local revenue would need to be replaced with sales taxes and property taxes being the most obvious potential sources.

“The world has changed. I feel it in the water. I feel it in the earth. I smell it in the air.” Galadriel in The Lord of the Rings: The Fellowship of the Ring (2001).

Local occupational taxes pose both a challenge and an opportunity for the Commonwealth to move forward; so, it makes sense for Kentucky to: provide for centralized filing for multijurisdictional filers; link the reference to the Internal Revenue Code to KRS 141.010; adopt single sales factor apportionment with market-based sourcing of KRS 141.120; and, shift away from local wages and net profits taxes.

About the author: Mark A. Loyd, JD, CPA, is a partner of Dentons Bingham Greenebaum LLP in Louisville and chairs its Tax and Finance group. Loyd chairs the Society’s Editorial Board. He can be reached at mark.loyd@dentons.com; 502.587.3552.